Why a HELOC Might Be Smarter Than a Full Refinance

When homeowners need extra cash, two common options come up:

- A full cash-out refinance (replacing your entire mortgage)

- A HELOC — Home Equity Line of Credit

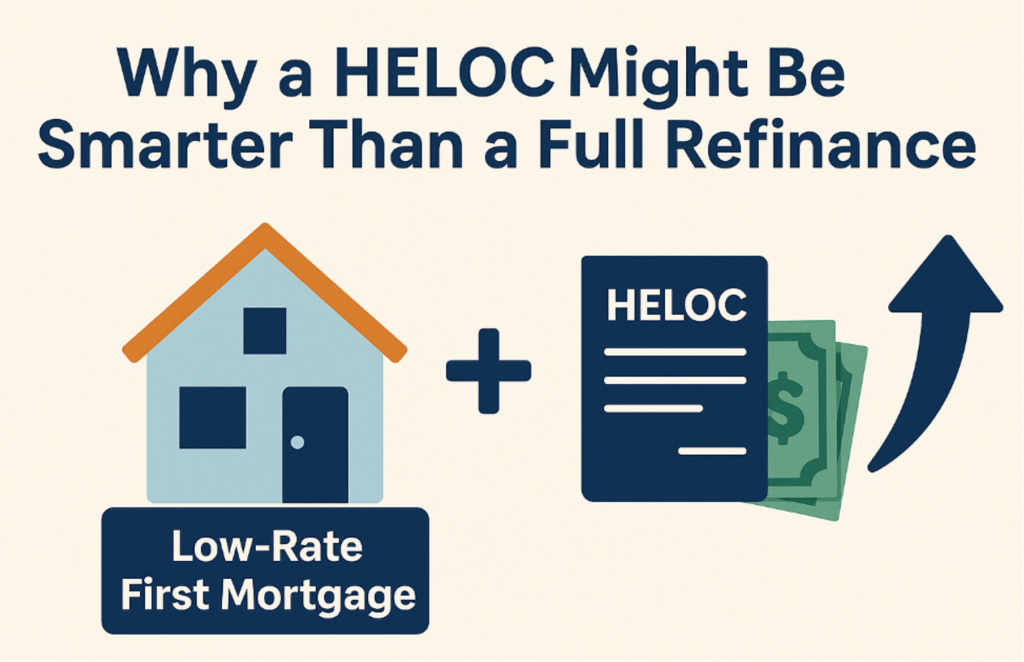

If your first mortgage already has a low rate, a HELOC can be the smarter move. Let’s break down why.

What Is a HELOC?

A HELOC works like a credit card, but it’s tied to the equity in your home.

- The bank or lender gives you a credit limit (for example, $50,000).

- You only make payments on what you actually borrow — not the whole limit.

- As you pay it back, you can borrow again (as long as you’re under your limit).

Example: If you have a $50,000 HELOC and you borrow $10,000 for a kitchen remodel, your payment is only based on that $10,000. If you pay it down to $5,000, you now have $45,000 available again.

Fixed vs. Adjustable Rate HELOCs

Not all HELOCs are the same:

- Adjustable-Rate HELOC: The interest rate changes based on the market. Payments can go up or down. Payments can be lower due to the interest only payment option mixed in with a 20-30 payment term option.

- Fixed-Rate HELOC: Some lenders let you “lock in” part or all of your HELOC balance at a fixed rate so your payments stay steady. Can be a higher payment due to lower terms of 5-15 year payment term.

Having both options means flexibility — you can float when rates are low or lock in if you want peace of mind.

Why Not Just Refinance?

If your first mortgage is at a low fixed rate (say 3%), refinancing into today’s higher rates (maybe 6–7%) doesn’t make sense. You’d raise the interest rate on your entire loan just to get cash out. Keep in mind though often times blending the rate depending on how much of a heloc you pull out, can make the overall rate higher, its best to consult with a mortgage broker for specifics on what your blended rate would be.

With a HELOC, you keep your low-rate mortgage in place and only borrow at today’s rate for the extra money you need. It can be cheaper and smarter.

What Can a HELOC Be Used For?

Homeowners often pull out a HELOC for:

- Home improvements (kitchen, bathroom, backyard)

- Paying off high-interest credit cards

- College tuition or education costs

- Big purchases or emergencies

- Starting a business

Since HELOC rates are often much lower than credit card rates (which can be 20%+), it can save thousands in interest.

Why Use a Mortgage Broker Instead of a Bank?

Working with a local mortgage broker it means:

- Faster closings — sometimes in as little as one week for our streamlined heloc product (banks can take 30–60 days).

- Streamlined process — less red tape, easier approval.

- More options — brokers work with multiple lenders to find the best fit.

Bottom Line

A HELOC can be a powerful financial tool when used wisely. It lets you access your home’s equity without giving up your low mortgage rate — and you only pay interest on what you actually use. Each scenario is different based on your circumstances, contact a mortgage broker to go over what would be your best option.

If you’re considering a HELOC, reach out to Jeanine Nucum – Your Local Mortgage Broker. I’ll walk you through the options, find the right fit, and help you access funds quickly and easily.